Etiqa has just launched their online investment offering, joining the ranks of other digital insurers that are seeking to reduce the costs for consumers that would otherwise be paid on their traditional counterparts.

But is it any good? I’ve scrutinised the details and will be providing a deeper look here for you.

Robo-advisory platforms (which invest in passively-managed ETFs) have been gaining popularity in recent years, but there are still many investors who prefer funds and unit trusts that are usually being actively managed to react to market conditions – especially for those who are too busy to manage their own investments and monitor market movements.

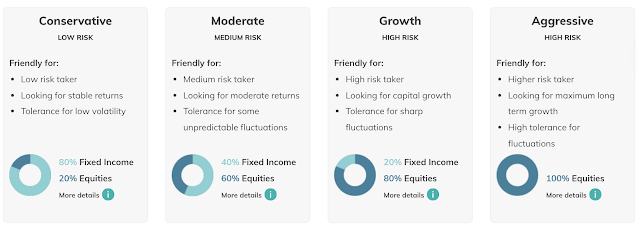

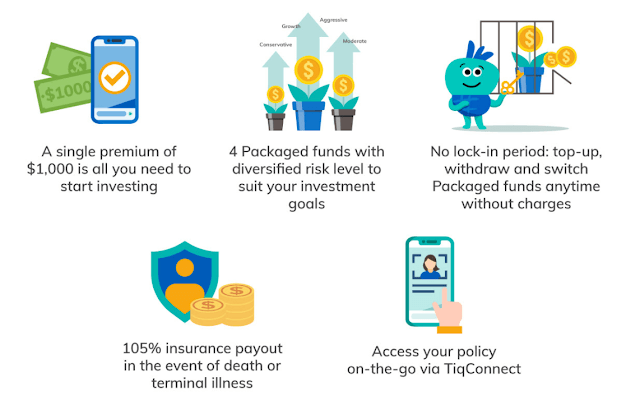

That’s one of the reasons why Etiqa has launched their newest investment product, Tiq Invest, which is designed with 4 different packaged funds that Etiqa has carefully selected to suit different risk appetites – from conservative to aggressive, and even one primarily focused on growth.

There is no lock-in period, meaning you can start with just a single premium of $1,000. If you’re a newbie who lacks the skill and time, you could still easily kick start your investments with this, without having to worry too much about how your portfolio is performing (since they’re being managed by professional fund managers).

What’s more, you can also employ dollar cost averaging through recurring top-ups based on your preferred frequency, though you should note that since that needs to be at least $100 per month, the minimum is thus $100 monthly / $300 per quarter / $600 for semi-annual / $1,200 per year.

What makes this better than traditional ILPs sold through agents is that you do not pay any insurance charges at all. This is important, because with 100% of your money invested upfront, you won’t be experiencing a scenario where your units will have to be sold to cover the increasing cost of your insurance over time – a feature that traditional ILPs suffered from. In the event of death or terminal illness, your loved ones will receive a lump sum payment of either 105% of net premiums paid or your account value – whichever is higher.

For those who don’t appreciate what this means, imagine this: even in the unfortunate situation where your funds don’t make money, your loved ones will STILL get the original capital that you’ve invested. This is NOT the case when you invest directly in the stock market, where no one will give your loved ones back your invested capital in the event of losses when they liquidate your portfolio after your death.

Your suitability for this product will be determined by an online Customer Knowledge Assessment (CKA) vs. the traditional way whereby an insurance agent assesses your suitability for an ILP.

Since there are no insurance agents who need to be paid for distributing the ILP to you, this method effectively removes middle man costs, which translates into lower charges for consumers. The fees are transparent, and Etiqa only imposes a management charge fee + fund management fee (i.e. the fee charged by the ILP sub-fund managers like BlackRock or Dimensional Fund Advisors Ltd). The current fund management fee is at 1.55%, which has already been calculated into your daily packaged fund unit price (see here for more information). There is no bid offer spread charge, and all unit pricing is based on a bid-to-bid basis.

What exactly will my money be invested into?

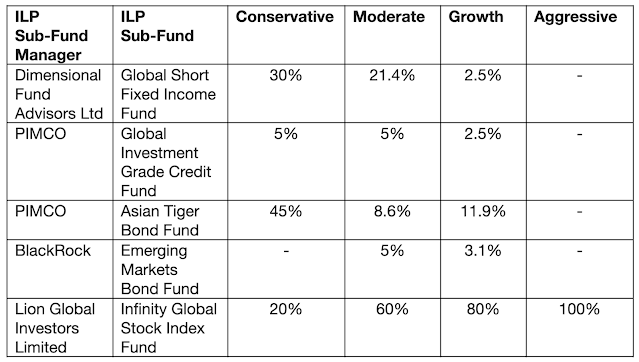

The 4 Packaged funds are put together using a combination of 5 different ILP sub-funds, which are consolidated in the table below for your reference:

As you can see, the allocation to equities increases as you tune up the risk aggression level. And for investors who cannot withstand too much volatility and risk in their portfolio, the conservative option will only have a 20% exposure to equities, while 3/4 is invested in Asian bonds and fixed income instruments. For the Asian bonds, no more than 20% is exposed to China’s funds.

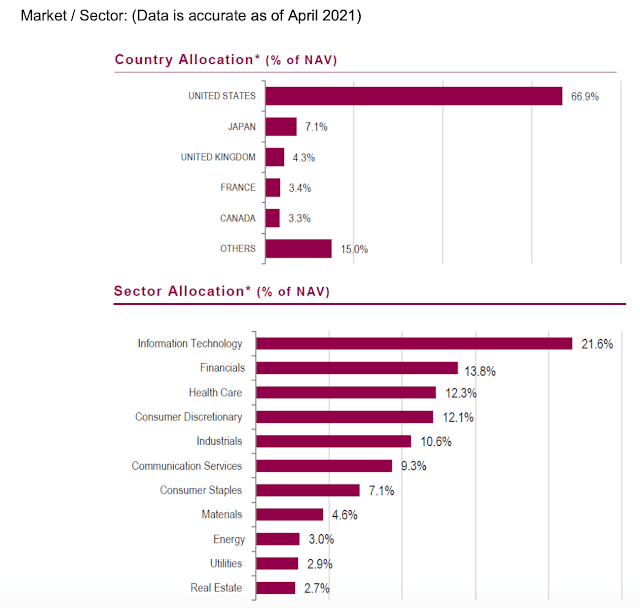

For the Aggressive portfolio, 100% is invested in equities that track the MSCI World Index – meaning that at time of writing, your largest exposure will be to Apple, Microsoft, Amazon, Facebook, Google and Tesla, just to name a few.

Source: Tiq Invest Fund Summary

Changed your mind on your risk appetite? No worries, Tiq Invest allows for unlimited packaged fund switches with no charges while your policy is in force. The only thing to note is that they’ll sell all your existing units and buy into the new fund that you’ve told them to switch to, instead of deducting or incrementally adding units until the fund allocations are met.

Tiq Invest vs DIY

Of course, if you’re a savvy investor who’s already managing your own portfolio, then this product won’t appeal to you, and probably wouldn’t be suitable anyway.

But aside from the insurance perks (remember how your loved ones will still get back your invested capital even if your account value has dropped, because of the coverage protection by Etiqa?), I can also see 2 other reasons why someone might choose Tiq Invest instead of doing it himself manually.

Rebalancing will automatically be carried out on your behalf on a periodic basis to ensure these allocations remain somewhat constant. This saves you the time, effort and also transaction fees that you would otherwise have to pay if you were a DIY investor. In the event of any payouts from an ILP sub-fund, the dividends will also be automatically reinvested back into the packaged fund for you.

How much will you have to pay Etiqa for managing the above for you? Well, that will be a flat rate of 0.75% per annum of your account value. This is where Tiq Invest mainly differs from other insurers who calculate the fund management fee they charge based on each individual ILP sub-fund (different rates for different ILP sub-funds). Note that even in the event of any changes, Tiq’s fund management fee is capped at 4% per annum of your account value.

At only 0.75% per annum, Tiq Invest charges lower than other digital ILPs in the market (which are 0.25% per quarter, meaning you pay 1% in total each year).

Conclusion

ILPs can still serve a small and niche market for those who prefer to have someone else manage their investments for them. Of course, this will naturally come at a higher cost than if you DIY, but if you feel your time and energy is better spent elsewhere (such as working on your business, or clocking in more hours at your high-income job, or even with your family), then Tiq Invest could be one option for you to consider.

Find out more about digital ILPs and sign up online today at Tiq Invest.

[End]

Tiq Invest is underwritten by Etiqa Insurance Pte. Ltd. (Company Reg. No. 201331905K).

Tiq Invest is an Investment-linked Plan (ILP) which invest in ILP sub-fund(s). Investments in this plan are subject to investment risks including the possible loss of the principal amount invested. The performance of the ILP sub-fund(s) is not guaranteed and the value of the units in the ILP sub-fund(s) and the income accruing to the units, if any, may fall or rise. Past performance is not necessarily indicative of the future performance of the ILP sub-fund(s).

A product summary and product highlights sheet(s) relating to the ILP sub-fund(s) are available and may be obtained from us via www.tiq.com.sg/product/tiqinvest. A potential investor should read the product summary and product highlights sheet(s) before deciding whether to subscribe for units in the ILP sub-fund(s).

As buying a life insurance policy is a long-term commitment, an early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid. You should seek advice from a financial adviser before deciding to purchase the policy. If you choose not to seek advice, you should consider if the policy is suitable for you.

This content is for reference only and is not a contract of insurance.

Full details of the policy terms and conditions can be found in the policy contract.

This policy is protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us or visit the Life Insurance Association (LIA) or SDIC web-sites (www.lia.org.sg or www.sdic.org.sg).

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Information is accurate as at a 19 August 2024.

This article was first published OCT 3, 2021, by Budget Babe. You can see the original article here. All information is correct as at the date of publication.