1 In 4 Or 5 Singaporeans

get diagnosed with a critical illness in their lives1. Don’t let critical illness set you back from your aspirations and retirement goals.

More Than 90% Of Severe Stage Critical Illness Claims

come from five conditions2. This includes major cancer, heart attack of specified severity, and stroke with neurological deficit.

Higher Critical Illness Survival Rates

Medical advancements have increased critical illness survival rates3 – You may want to consider preparing for the cost of surviving a critical illness.

100% Payout

Paid to you in a lump sum that you can use on medical and living expenses.

No Medical Examinations

Save time on medical exams. Pass 3 health questions to qualify. Your family history doesn’t matter to us.

High Coverage of Up to $300,000 Sum Insured

Choice of coverage from S$30,000 - S$300,000. Get this as your first critical illness plan or as added coverage.

Gender

Have you smoked in the last 12 months?

Date of Birth

Select your coverage

Enter any amount from S$30,000 to S$300,000

The Basic Financial Planning guide recommends Critical Illness protection equivalent to 4x your annual income. Learn more

Have a promo code?

Find out how much it cost

Premium starting from

or

Premium starting from

S$ - /month

or

S$ - /year

Premium starting from

or

Yearly Renewable Coverage Up To Age 85

No medical examinations required to have your coverage renewed every year up to age 85. Whether you’re 18 or 70, you can buy Tiq 3 Plus Critical Illness if you pass 3 simple health questions.

Death Coverage Included

Tiq 3 Plus Critical Illness also provides S$20,000 lump sum benefit for your loved ones in the event of your death. This death benefit extends to you and up to 4 of your children5.

Expand Your Heart & Neurological Coverage

Our optional Heart & Neurological Disorder Rider gives you greater coverage. It goes beyond severe stage heart attacks and strokes.

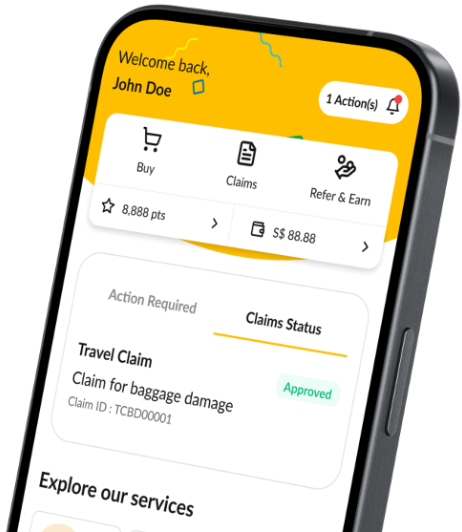

Download the Etiqa+ SG App

Create your account in minutes.

Submit your claim and supporting documents

Login to your account and submit them via the Etiqa+ SG App.

Sit back and let us do the heavy lifting

Our claims assessor will review your claims.

Your claims are ready

Once your claim is successfully approved, you will be notified via SMS and/or email.

Product Summaries

Promotion Terms & Conditions:

Be the first to know

Get the latest promotions and news

I consent and agree for Etiqa Insurance to collect, use and disclose the personal data above for the purposes of validation and sending, via telephone calls and text message. Read Etiqa's Privacy Policy [here]