Wondering how to avoid emotional investing and stay rational when the markets go crazy? Dollar-cost averaging (DCA) could be your answer.

Earlier this month, companies in China whose names resemble Eileen Gu – gold medal winner at Beijing Winter Olympics 2022 – enjoyed a surge due to a spill over effect from the sportswoman’s newfound popularity. When money is involved, it can be difficult to stay rational. It’s a known fact that emotions affect decision-making and that extends to all aspects of life, even in investing!

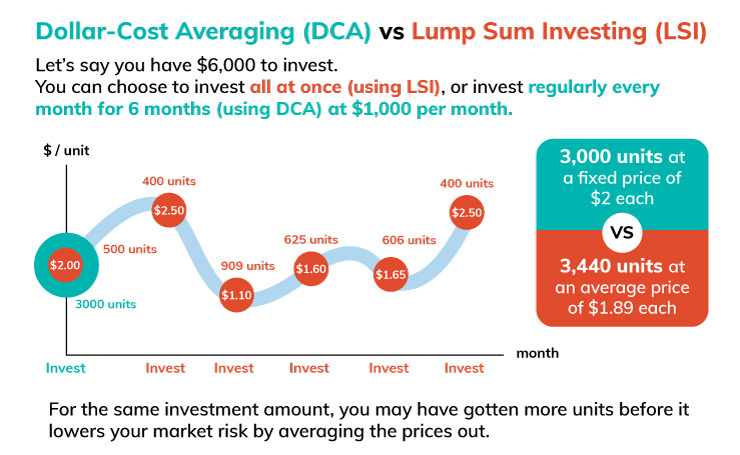

The good news is, there are investment strategies such as dollar-cost averaging that can help you to stay rational. We will also be sharing on lump sum investing, since many of you ask about the difference between the two.

What is dollar-cost averaging (DCA)?

“Studies have shown that DCA works to spread out your risk. This is especially relevant in today’s market where we see heightened volatilities as policy makers and/or central bankers attempt to control inflation while COVID-19 pandemic continues and recently, geopolitical tensions in Ukraine.” — Alan Koay, Head of Investment, Etiqa Insurance

Have you watched one of those Hong Kong comedies featuring a stock market prodigy when you were growing up? In these cookie-cutter movies, the main lead would somehow get inspired and invest randomly in a particular stock. That’s NOT dollar-cost averaging.

Consistency is the key of dollar-cost averaging, where one invests a fixed sum of money into a particular investment at regular intervals, typically monthly or quarterly.

The DCA investment strategy allows the investor to divide the total sum to be invested across periodic purchases of a target asset, so as to reduce the impact of volatility on the overall purchase. The purchases occur regardless of the asset’s price and at regular intervals.

With this formula set in place, investors continue to invest regardless of the market’s short-term movements – hence staying rational even in times of volatility.

What is lump sum investing (LSI)?

As the name suggests, lump sum investing (LSI) is like that movie analogy that we mentioned previously – where an investor puts all his/her money into the market as soon as possible. This is common, especially when stock prices are deemed to be falling or lower than their actual value.

If you are someone who’s prone to anxiety, LSI may not be a suitable investment strategy for you since market fluctuations may cause short-term losses and make you constantly second-guess your decision.

Dollar-cost averaging (DCA) vs lump sum investing (LSI)

| Dollar-cost averaging | Lump sum investing |

| $$$ Lower expected returns |

$$$$$ Higher expected returns |

| This study shows that lump sum investing works better based on investments across 10-year periods. When markets are going up, you can take full advantage of the market growth by putting your money to work right away. | |

|

|

More on dollar-cost averaging

Have you wondered why there seems to be an investment hype in recent years? Investing may seem new to you but it actually goes back to the early 17th century. In fact, there have been many research done on investment strategies, and the Vanguard’s study in particular shares interesting insights on the dollar-cost averaging strategy.

The study found that during a down market (kind of like our current market that’s affected by war), dollar-cost averaging resulted in losses less frequently than lump sum investing. Specifically, the study found that lump sum investing declined in value 22.4% of the time. Dollar-cost averaging was down 17.6% of the time.

Hence, dollar-cost averaging would be more suitable for investors who are less risk-averse. It allows investor of all levels, especially new investors, to get comfortable with the markets.

What is the best way to dollar-cost average?

For new investors, the term “dollar-cost averaging” may sound foreign, and even seems intimidating. However, it is actually pretty easy to execute. Here’s how you can easily go about it:

- Start early

Similar to the idea of investing as early as you can, you shall be able to enjoy compounding returns when you start early. The time value of money increases over a period of time and your regular investments made right from an early age can lead to lower risks and greater returns in the long run.

- Invest consistently

Consistency is the key to dollar-cost averaging. Investing consistently means that you invest the same amount of money regularly at a particular frequency, e.g. investing $100 every month into the same packaged funds regardless of market movements. To begin, you should decide how much you want to invest, how often you want to invest, the periods you want to split your investments over, and then, stick to the plan.

In case you are thinking that this is troublesome and you are likely to miss an investing cycle, there are certain investment tools such as Tiq Invest with automated recurring top-up features that you can pre-set to enable the easy execution of dollar-cost averaging. In such cases, you don’t need to worry about investing late (we know it happens sometimes).

- Be aware of costs

Dollar-cost averaging requires buying units regularly and trading. In such cases, transaction fees can add up for certain products. While it is good to mitigate risks, you want to ensure that the fees are not eating into your potential returns.

Tiq Invest does not impose additional fees for fund switching. In fact, our management charge fee at 0.75% per annum of your account value is one of the lowest1 in the market. Hence, you can easily apply the dollar-cost averaging strategy without worries of hefty fees when you invest with Tiq Invest.

Does dollar-cost averaging work?

Dollar-cost averaging is favoured by investors with lower risk tolerance, as it can help one to avoid timing the market and take the emotion out of investing. On the flip side, there’s the opportunity cost of forgoing the potential for higher returns. To decide on whether it is suitable for you, you need to look into your investment objectives.

Last but not least, constant research and monitoring can help keen investors to make more informed decisions. However, you should keep in mind that it is challenging to predict the market because nobody knows what the future harbours

[End]

1 Based on the available digital Investment-Linked Plan (ILP) as at 19 August 2024. This comparison does not include information on all similar products. Etiqa Insurance Pte Ltd does not guarantee that all aspects of the products have been illustrated. You may wish to conduct your own comparison for products that are listed in www.comparefirst.sg.

Information is accurate as at 19 August 2024. This policy is underwritten by Etiqa Insurance Pte. Ltd. (Company Reg. No. 201331905K).

Tiq Invest is an Investment-linked Plan (ILP) which invest in ILP sub-fund(s). Investments in this plan are subject to investment risks including the possible loss of the principal amount invested. The performance of the ILP sub-fund(s) is not guaranteed and the value of the units in the ILP sub-fund(s) and the income accruing to the units, if any, may fall or rise. Past performance is not necessarily indicative of the future performance of the ILP sub-fund(s).

A product summary and product highlights sheet(s) relating to the ILP sub-fund(s) are available and may be obtained from us via www.tiq.com.sg/product/tiqinvest. A potential investor should read the product summary and product highlights sheet(s) before deciding whether to subscribe for units in the ILP sub-fund(s).

As buying a life insurance policy is a long-term commitment, an early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid. You should seek advice from a financial adviser before deciding to purchase the policy. If you choose not to seek advice, you should consider if the policy is suitable for you. This content is for reference only and is not a contract of insurance. Full details of the policy terms and conditions can be found in the policy contract.

This policy is protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us or visit the Life Insurance Association (LIA) or SDIC web-sites (www.lia.org.sg or www.sdic.org.sg).

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Tiq by Etiqa Insurance Pte. Ltd.

A digital insurance channel that embraces changes to provide simple and convenient protection, Tiq’s mission is to make insurance transparent and accessible, inspiring you today to be prepared for life’s surprises and inevitabilities, while empowering you to “Live Unlimited” and take control of your tomorrow.

With a shared vision to change the paradigm of insurance and reshape customer experience, Etiqa created the strong foundation for Tiq. Because life never stops changing, Etiqa never stops progressing. A licensed life and general insurance company registered in the Republic of Singapore and regulated by the Monetary Authority of Singapore, Etiqa is governed by the Insurance Act and has been providing insurance solutions since 1961. It is 69% owned by Maybank, Southeast Asia’s fourth largest banking group, with more than 22 million customers in 20 countries; and 31% owned by Ageas, an international insurance group with 33 million customers across 16 countries.

Discover the full range of Tiq online insurance plans here.