Hospitalisation in Singapore can be costly, even with MediShield Life or a private insurance plan. To better manage expenses, many Singaporeans buy Integrated Shield Plan (IP) riders. This optional add-on helps reduce out-of-pocket costs, including deductibles and co-insurance during hospitalisation. If you’re planning to review, renew, or buy coverage, start by understanding how IP riders work, and the key changes coming into effect from 1 April 2026 under the Ministry of Health (MOH)’s new design requirements.

What Are IP Riders? A Quick Refresher

IP riders are optional add-ons to your Integrated Shield Plan, which complements your MediShield Life coverage. They help lower the amount you pay out of pocket when you are hospitalised, especially for larger bills or private care. Here’s how IP riders work:

- Cover the minimum deductible: This is the fixed amount you need to pay before your insurance policy begins to pay. The deductible can go up to a few thousand dollars depending on your ward class, so having a rider helps ease the upfront financial burden during hospitalisation.

- Reduce co-insurance costs: This is the percentage of hospital bills you would otherwise pay (typically 3-10%). IP riders lower this share, which can make a substantial difference for high medical bills, helping you keep more of your savings intact.

- Support coverage for higher ward classes or private hospitals, depending on the plan you hold

Overall, IP riders are particularly useful if you plan to seek treatment in higher ward classes (such as A or private wards) or want stronger protection against large hospital bills.

Key Changes

From 1 April 2026, all new IP riders sold in Singapore will see some important updates:

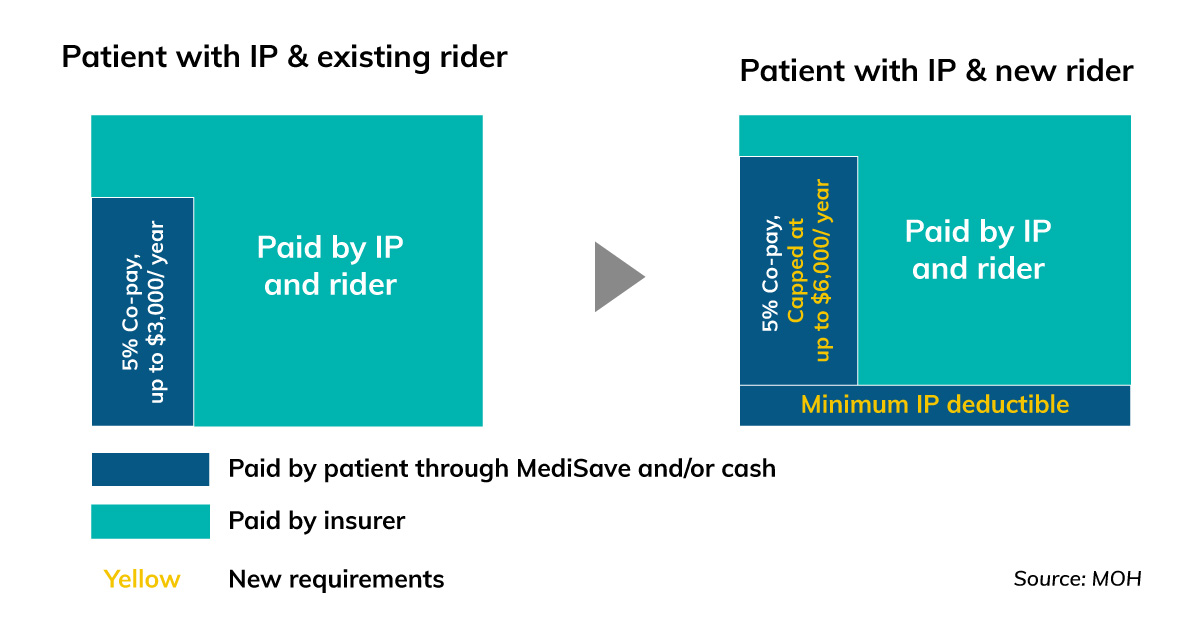

| Feature | Before | From 1 April 2026 | What This Means for You |

| Coverage for Minimum Deductible | Riders could cover the minimum deductible (up to ~$4,500 depending on ward class) | Riders no longer cover the minimum deductible set by MOH | You will pay the deductible out-of-pocket before insurance payouts begin |

| Co-Payment Cap (Annual Limit) | At least $3,000 per policy year (excluding deductible) | Increased to at least $6,000 per policy year (excluding deductible) | Your maximum annual co-payment may be higher if hospitalised |

| Minimum Co-Payment Requirement | 5% co-payment | No change – 5% minimum still applies | You will continue to share part of the bill |

| Protection Against Large Bills | Riders reduce exposure to large hospital bills | Riders still protect against major medical expenses | Protection remains, but you bear a larger portion upfront compared to older rider designs |

Here’s a simplified diagram for you to visualise the changes:

How to Think About Your Coverage Strategy

Although premiums under the new IP rider design may be lower, policyholders should be prepared for higher out-of-pocket costs when hospitalised. Despite these changes, IP riders remain a valuable safeguard against large medical bills. Here are some practical strategies to help you make the most of your coverage:

1. Ward Choice Matters

Ward choice plays an important role in determining your coverage and premiums. IP benefits depend on your selected ward class; essentially the level of hospital ward you prefer and would like your plan to cover up to, such as Private, A, B1, or B2/C.

Choosing a higher ward class coverage generally means higher premiums but offers greater comfort and more flexibility in selecting doctors. Conversely, opting for lower ward classes provides stronger government subsidies and lower hospital bills, though waiting times may be longer.

When deciding, it’s important to balance your personal comfort, tolerance for waiting, and overall budget to ensure your ward choice aligns with both your medical and financial priorities.

2. Assess Your Budget

When assessing your health insurance budget, remember that premiums generally rise with age and higher coverage levels.

- Plan for rising premiums over time: Insurers adjust premiums based on age bands and coverage tiers. Higher ward classes and riders increase long-term costs.

- Prepare for out-of-pocket medical expenses: Deductibles and co-payments may still apply. Set aside emergency funds to avoid financial strain during hospitalisation.

- Account for major financial commitments: Consider your mortgage, dependents, and daily expenses. Ensure your premiums remain manageable alongside these obligations.

- Prioritise long-term affordability: Choose a plan you can sustain over the years. Avoid over-insuring if it risks affecting your retirement savings or financial stability.

Balancing coverage and affordability helps you stay protected without compromising your overall financial wellbeing.

3. Use MediSave Smartly

MediSave is a powerful tool to help manage your health insurance costs, especially for hospitalisation. Use it to strategically maintain continuous coverage.

You can use it to pay premiums for MediShield Life within the age-based withdrawal limits set by the MOH. Plan your usage carefully to avoid shortfalls and keep your coverage active. Each age group has a fixed withdrawal cap. Monitor your MediSave balance regularly to ensure you can fully cover your premiums each year without disruption.

In addition, MediSave can sometimes be used to pay premiums for certain family members. This helps you manage your household’s healthcare costs more efficiently. Maintain a healthy MediSave balance over time. This ensures you have sufficient funds when hospitalisation or major treatments occur.

4. Additional Coverage Options

While IP riders primarily help reduce out-of-pocket costs for hospital bills, they mainly cover medical treatment expenses. They may not address other financial pressures that can arise if you are diagnosed with a serious illness.

This is where critical illness plans can play an important role. These plans provide a lump-sum payout upon diagnosis of a covered condition, such as cancer, heart attack, or stroke. Unlike hospitalisation plans that reimburse specific medical bills, the payout from a critical illness policy can be used more flexibly – whether for ongoing living expenses, rehabilitation, or replacing income if you need time away from work.

There are also cancer-specific plans that focus on coverage for this particular condition. These plans may provide financial support at different stages, from diagnosis to treatment and recovery, helping to ease the financial strain during what can be a challenging time.

By complementing your hospitalisation coverage with critical illness protection, you can build a more comprehensive financial safety net that helps cover both medical expenses and the wider financial impact of serious illness.

Other Helpful Tips to Consider

When comparing insurance options, don’t focus solely on premiums. Examine coverage limits, benefits, exclusions, and policy conditions, as these determine how much protection you actually receive when a claim arises.

Some insurers may adjust premiums over time based on factors such as age bands, claims experience, or medical cost trends. Reviewing these aspects early can help you choose a plan that remains sustainable in the long run.

Consider your personal health risk profile, including age, family medical history, and lifestyle. This helps you select coverage that meets your needs. If you need flexibility in hospital choice or specialist care, factor this into your decision to maximise convenience and peace of mind.

Conclusion

The health insurance landscape continues to evolve, making it important to review your coverage from periodically. Major life events such as starting a family, changing jobs, or changes in your healthcare needs may affect the level of protection that best suits you. Taking time to reassess your plan can help ensure your coverage remains relevant and minimise potential gaps in protection.

If you are unsure about specific policy details, it is a good idea to speak directly with your insurer for clarification. Should you have any questions, you may reach out to our assurance managers at +65 6887 8770, who will be happy to assist you.

[End]

Important notes:

These policies are underwritten by Etiqa Insurance Pte. Ltd. This content is for reference only and is not a contract of insurance. Full details of the policy terms and conditions can be found in the policy contract. The information contained on this product advertisement is intended to be valid in Singapore only and shall not be construed as an offer to sell or solicitation to buy or provision of any insurance product outside Singapore.

As buying a life insurance policy is a long-term commitment, an early termination of the policy usually involves high costs and the surrender value, if any, that is payable to you may be zero or less than the total premiums paid. As term life insurance has no savings or investment feature, there is no cash value if the policy ends or if the policy is terminated prematurely.

You should seek advice from a financial adviser before deciding to purchase the policy. If you choose not to seek advice, you should consider if the policy is suitable for you.

These policies are protected under the Policy Owners’ Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us or visit the Life Insurance Association (LIA) or SDIC websites (www.lia.org.sg or www.sdic.org.sg).

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Information is accurate as at 1 April 2026.

Tiq by Etiqa Insurance Pte. Ltd.

A digital insurance channel that embraces changes to provide simple and convenient protection, Tiq’s mission is to make insurance transparent and accessible, inspiring you today to be prepared for life’s surprises and inevitabilities, while empowering you to “Live Unlimited” and take control of your tomorrow.

With a shared vision to change the paradigm of insurance and reshape customer experience, Etiqa created the strong foundation for Tiq. Because life never stops changing, Etiqa never stops progressing. A licensed life and general insurance company registered in the Republic of Singapore and regulated by the Monetary Authority of Singapore, Etiqa is governed by the Insurance Act and has been providing insurance solutions since 1961. It is 69% owned by Maybank, Southeast Asia’s fourth largest banking group, with more than 22 million customers in 20 countries; and 31% owned by Ageas, an international insurance group with 33 million customers across 16 countries.

Discover the full range of Tiq online insurance plans here.